Options Pricing Monte Carlo

Options Pricing Monte Carlo Summary

Options Pricing Monte Carlo is a with in-app purchases iOS app in Finance by Tenacious App Production, LLC. Released in Mar 2018 (8 years ago). It has 3.00 ratings with a 5.00★ (excellent) average. Based on AppGoblin estimates, it reaches roughly 17 monthly active users and generates around $<10K monthly revenue (100% IAP / 0% ads). Store metadata: updated Feb 26, 2021.

Store info: Last updated on App Store on Feb 26, 2021 .

5★

Ratings: 3.00

Screenshots

App Description

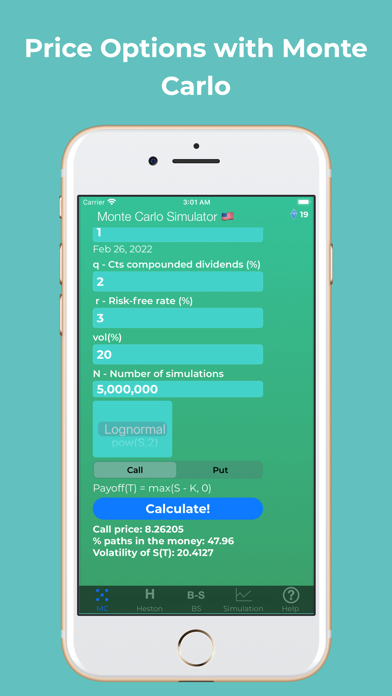

The Options Pricing Monte Carlo app prices power options: max(S^i -K,0) or max(K-S^i,0). It also shows the % of paths with positive payoffs. The normal inverse is calculated with Beasley-Springer-Moro method.

The Heston tab is used to price options under stochastic volatility using Monte Carlo.

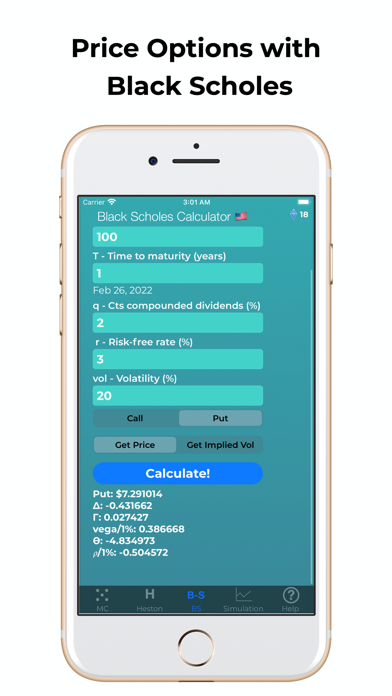

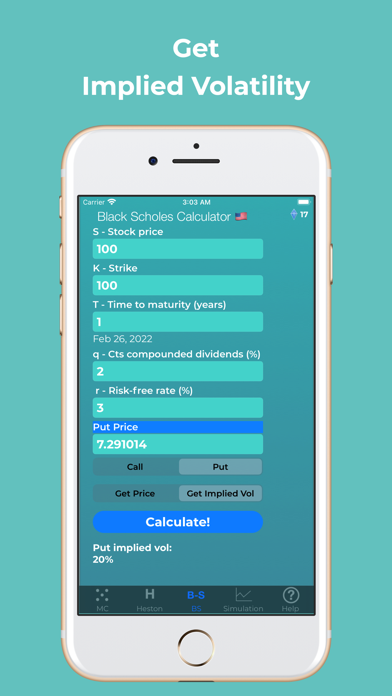

It also prices European options using Black-Scholes and can also calculate Implied Vol. Normal is calculated by direct integration using Simpson method with a low tolerance.

So 4 calculators in one:

- Monte Carlo simulator for regular European and Power options.

- Monte Carlo simulator for European options with stochastic vol (Heston model).

- Black Scholes calculator for price and greeks and implied vol.

- Simulation tab lets you visualize Brownian Motion with drift. (2D or vs time).